|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

| |

|

|

|

|

|

|

| |

| |

News Articles |

|

| |

| The 2018 investment year |

|

|

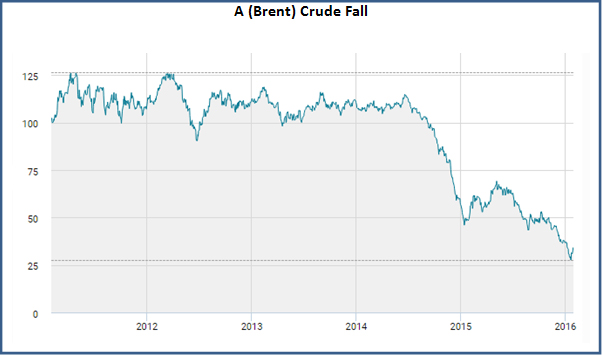

The world’s share markets mostly saw falls in 2018.

Index |

2018 Change |

FTSE 100 |

-12.5% |

FTSE All-Share |

-13.0% |

Dow Jones Industrial |

-5.6% |

Standard & Poor’s 500 |

-6.2% |

Nikkei 225 |

-12.1% |

Euro Stoxx 50 (€) |

-14.3% |

Shanghai Composite |

-24.6% |

MSCI Emerging Markets (£) |

-11.5% |

2018 was a very different year for investors from 2017. During that year, the share markets generally produced positive returns with very little volatility. Both years had their fair share of dramas, with Brexit and Donald Trump sources of concern across the 24 months. However, whereas in 2017 stock markets seemed relatively unphased by events, the opposite was true in 2018.

In sterling terms, the MSCI World Index was down 4.9%, much less than the main UK indices. However, this hides two factors:

1. The US stockmarket, which forms about half of the World Index, was relatively strong. Strip that out and the MSCI World Index ex-USA was down 11.2% in sterling terms, only marginally less than the main UK indices.

2. The Brexit-battered pound was weak during 2018, which flattered overseas returns.

|

|

|

|

|

| |

| Filling the pensions hole for the self-employed |

|

|

The Department for Work and Pensions (DWP) is aiming to expand pension coverage among the self-employed.

Pension automatic enrolment has become a major success since it was launched nearly seven years ago, with almost 10 million people joining a workplace pension arrangement. Take-up rates have been much higher than some pundits had forecast – the latest calculation from the DWP showed that in 2016/17 the overall opt out rate was just 9%.

However, there is one group of people that the automatic enrolment regime completely misses: the self-employed. According to the DWP, the self-employed account for about 15% of the UK workforce – 4.7 5 million people. Private pension coverage in this sector is low, despite the tax benefits on offer. The DWP has calculated that in 2016/17, only about 1 in 7 of the self-employed were saving into a pension.

Encouraging pension saving

In December the DWP announced that it would be running a programme of trials aimed at encouraging the self-employed to start saving. These trials will involve a range of trade bodies and financial services organisations, including the main government initiated auto-enrolment scheme, NEST, which now has over seven million members.

|

|

|

|

|

| |

| Understanding the Child Benefit Charge |

|

|

7 January marked the fifth anniversary of the tax on child benefits, an imposition that is still not widely understood.

The High Income Child Benefit Charge (HICBC), to give child benefit tax its correct name, was introduced in a rush by George Osborne – so much so that it began three months before the start of the 2013/14 tax year. It was, and remains, a classic example of the type of tax system tweaking beloved of Chancellors and disliked by those who have to deal with the consequences.

The HICBC represented an attempt to use the income tax system to withdraw child benefit from parent(s) (married or not) where one had income exceeding £50,000. Its introduction was poorly publicised, leaving many people – particularly PAYE earners – unaware of their potential liability.

Caught by ‘failure to notify’?

If proof were needed of the flaws in HICBC, it arrived in November 2018. That was when HMRC announced it would be reviewing ‘Failure to Notify” penalties for 2013/14, 2014/15 and 2015/16 “to customers [sic] who did not register for the High Income Child Benefit Charge” and therefore did not pay the HICBC tax. Unusually for HMRC, it is not looking for the taxpayer to provide a “reasonable excuse” before considering a refund. It may be hoping to avoid a flood of letters from those affected.

The income trigger for the HICBC remains at £50,000. That means that for 2019/20 the trigger matches the UK higher rate threshold. When it began, the charge started at over £7,500 above the then threshold.

|

|

|

|

|

| |

| Shake up your New Year’s resolutions |

|

|

The time to resolve has returned.

Have your New Year resolutions fallen by the wayside yet? You know, the ones about eating better, drinking less and exercising more. The problem is they all require you to make a change to your lifestyle, which is never easy, particularly in the dark days of mid-winter.

Some people prefer to talk about intentions rather than resolutions. And to try to look beyond the short-term goals to longer term outcomes to boost the likelihood of sticking to them.

Here are four simple financial New Year’s resolutions. They need only one-off actions, so they should be easier to stick to. And they could provide long term benefits:

1. Make a will. If you don’t have a will, you have no say in how your estate is distributed. That may not matter if the laws of intestacy match your wishes, but often the two diverge considerably, leaving difficult issues for your dependants. If you have made a will, you are not completely off the hook: resolve to look at it and make sure it is still the right will for your current circumstances.

2. Set up lasting powers of attorney. Who would make decisions about your finances and medical treatment if you were unable to do so? Just as with a will, a lasting power of attorney lets you decide the answer rather than falling back on what the state determines or leaving your family without the ability to really help you.

3. Check what you are earning on your deposits. Many banks and building societies continue to pay negligible rates on accounts that are “no longer available” to new savers. Just because an account has ‘gold’ in its title is no guarantee that it won’t be paying a mere 0.1%.

4. Check your state pension entitlement. This is easy to do online (https://www.gov.uk/check-state-pension) and shows both what you should receive based on current rates and when you should start to receive it. The projection will also indicate any scope you have for increasing your state pension.

|

|

|

|

|

| |

| New earnings thresholds for auto-enrolment |

|

|

In early December the Department for Work and Pensions (DWP) announced the thresholds that should apply to automatic enrolment pension contributions from 6 April 2019. We say ‘should’ because, strictly speaking, they need final approval from the Secretary of State, although any change is extremely unlikely.

There are three key levels to be aware of:

• The Earnings Threshold This is the trigger level of earnings which brings a ‘worker’ into automatic enrolment. It used to match the personal allowance, but since 2015/16 has been frozen at £10,000. That round number will stay in place for the coming tax year.

• The Qualifying Earnings Lower Limit This is the floor level of earnings above which contributions are payable, but only if the earnings threshold is triggered. It matches the lower earnings limit, which is a key level for social security benefit entitlement and will be £6,136 (£118 a week) in 2019/20, an increase of £104 (£2 a week)

• The Qualifying Earnings Upper Limit This is the upper level of earnings on which contributions are payable. In past years it has matched the UK higher rate threshold. The same will be true for 2019/20, despite the £3,650 increase in that threshold to £50,000. This is not good news for Scottish taxpayers, whose own higher rate (41%, not 40%) threshold for earned income is set to be £43,430 in 2019/20.

Increasing contribution rates

These numbers take on more significance for 2019/20, as the minimum total auto-enrolment pension contribution rate will increase from 5% to 8% of qualifying earnings. Of the 8%, the minimum payable by the employer will be 3%, meaning many employees will see their contribution rate jump from 3% to 5% – a two thirds rise. |

|

|

|

|

| |

| Office of Tax Simplification’s first report on inheritance tax |

|

|

The Office of Tax Simplification (OTS) has published the first part of its inheritance tax (IHT) simplification review.

The report highlights a variety of issues with the current IHT system:

• IHT returns are submitted for about half of all estates, even though tax is paid by less than 5%;

• Most of the paperwork cannot be completed and submitted online and is far from user-friendly;

• Probate is not normally granted until IHT has been paid, which can create difficulty for executors;

• The residence nil rate band, introduced in 2017/18, was widely criticised as being ‘very complex’, and disadvantaging those who do not have children and those who have not owned their own home.

The OTS made a key administrative recommendation: ‘The government should implement a fully integrated digital system for Inheritance Tax, ideally including the ability to complete and submit a probate application’. HMRC have already started such a project in 2014, and in April 2018 announced it would be delayed, choosing instead to focus on the short IHT205 form which applies to certain estates where no IHT is payable.

|

|

|

|

|

| |

| Index-linked savings certificates |

|

|

The popular National Savings & Investments (NS&I) savings certificates will be indexed to CPI instead of RPI from next year.

The certificates have not been on sale since 2011, but NS&I allow existing certificate holders to reinvest in new series of certificates when their old ones mature. The terms have gradually worsened over the years and at present reinvestment promises a return of RPI inflation +0.01% a year. For certificates maturing from 1 May 2019, the basis of indexation will change from RPI to CPI.

The change was not picked up by newspapers at the time because they were released the Friday before the 2018 Budget, held on the Monday. Government departments are often accused of burying bad news, and the downgrading of the NS&I index-linked savings certificates is certainly bad news for affected investors.

|

|

|

|

|

| |

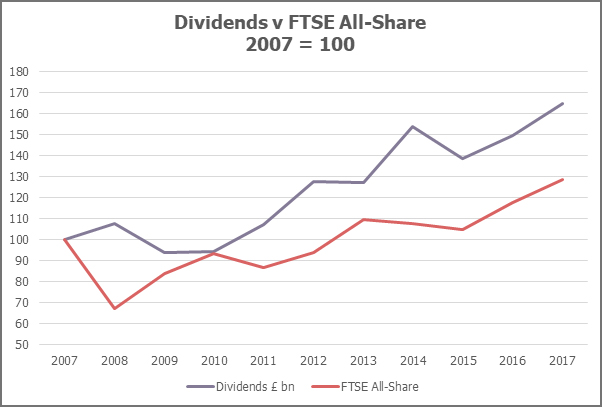

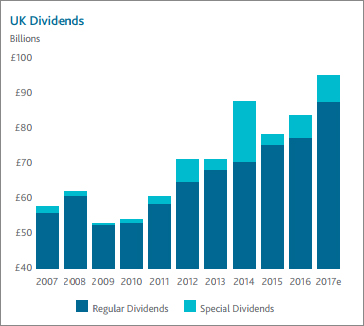

| UK dividends remain strong despite volatile markets |

|

|

UK dividends are continuing to grow faster than inflation, according to the latest quarterly data from Link Asset Service.

Source: Link Asset Services, FTSE

The latest UK Dividend Monitor (UKDM) shows that in the third quarter of 2018 dividend payments were 4.1% up on the previous year, comfortably above the current rate of inflation. Looking over the 10-year period from the end of 2007 to the end of 2017, total dividend payments have risen by an average of 5.1% while CPI inflation has averaged 2.4%.

The UKDM is published by Link Asset Services (formerly produced by Capita) and totals the dividends paid out on the ordinary shares of companies listed on the UK Main Market every quarter – excluding investment companies, to avoid double counting. It captures both regular dividends and one-off special dividends, which often stem from takeovers or other corporate restructurings.

As the graph shows, over the last ten years, the amount paid out in dividends has grown faster than the capital value of shares. There are still dips, but between 2007 and 2017 the regular dividend total dropped only once, in the wake of the global financial crisis. The jump and dive between 2013 and 2015 is an aberration caused by a one-off £15.9 billion special dividend paid by Vodafone in 2014.

|

|

|

|

|

| |

| New probate fees to affect many estates |

|

|

The government has revived plans to raise probate fees in England and Wales.

A new, banded structure for probate fees in England and Wales is to be introduced, according to a written statement issued a week after the 2018 Budget by the Parliamentary Under Secretary of State for Justice.

The announcement comes after the absence of inheritance tax (IHT) reforms in the Budget, despite the Chancellor commissioning a review by the Office of Tax Simplification in January 2018. The only change to IHT announced in October was a small adjustment to the legislation for the residence nil rate band – this being such a complex piece of legislation, it had been wrongly drafted.

New fee structure

If new probate fees sound familiar, it is because a very similar announcement was made in March 2017. At the time the proposal provoked widespread criticism, because the higher levels were seen to be more of a new tax than a simple fee adjustment. In the event the planned change fell victim to the legislative logjam around the last General Election and disappeared.

Since then, the government has taken on board some of the original criticism and cut the fees they are proposing, particularly for larger estates:

Value of estate |

Old Proposal |

New Legislation |

Up to £50,000 or exempt from requiring a grant of probate |

Nil |

Nil |

£50,001 - £300,000 |

£300 |

£250 |

£300,001 - £500,000 |

£1,000 |

£750 |

£500,001 - £1,000,000 |

£4,000 |

£2,500 |

£1,000,000 - £1,600,000 |

£8,000 |

£4,000 |

£1,600,001 - £2,000,000 |

£12,000 |

£5,000 |

Over £2,000,000 |

£20,000 |

£6,000 |

|

|

|

|

|

| |

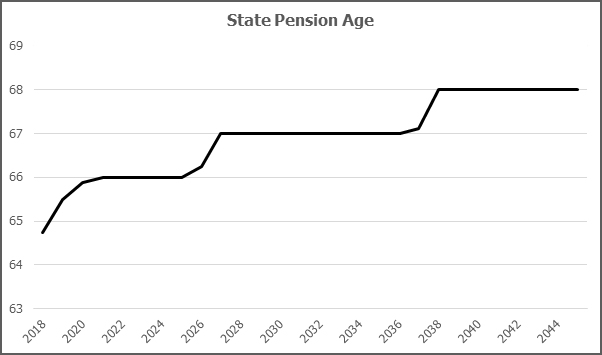

| State pension equality means increases for all |

|

|

The government has revived plans to raise probate fees in England and Wales.

Having reached this landmark, the next stage of SPA increases has already started. For both men and women, the state pension will become payable for anyone born between 6 December 1953 and 5 January 1954 on 6 March 2019. The SPA will then be increased to reach age 66 by October 2020.

The SPA is scheduled to rise again as existing legislation already covers the increase from 66 to 67, phased in over two years from April 2026. The same legislation provides for a step up to 68, starting in April 2044.

However, in July 2017 the Department for Work and Pensions announced it would accept the recommendations of the Cridland Review – this brings the start of the move to a SPA of 68 forward to April 2037. Legislation for this change has been deferred until after the next SPA review in 2023 – raising the SPA in the current political conditions could prove difficult for the government – but if your SPA will be at least 68 if you were born after 5 April 1971.

|

|

|

|

|

| |

| State pension sees rise thanks to the triple lock |

|

|

A 2.6% rise in the single tier state pension was announced in the 2018 Budget.

The increase to the single tier state pension, and its predecessor the basic state pension, will apply from next April. Other state pensions, such as the State Earnings Related Pensions Scheme (SERPS), will rise by 2.4%.

The higher increases for the two main pension benefits are the result of the ‘triple lock’, which requires the annual uplift to be greatest of:

• CPI inflation (2.4% in September 2018);

• Earnings inflation (2.6% for average weekly earnings to July 2018); and

• 2.5%.

The increased payment – £4.30 a week for the single tier pension – is often presented as extra money for pensioners. However, it is doing little more than maintaining the state pension’s buying power against inflation.

Earnings and CPI inflation have been roughly in line with each other for some time, which can be linked to any discussion about the lack of real wage growth. Had September’s annual inflation figure come in at 2.6%, as expected by many pundits, it would once again have been the triple lock winner, albeit matched by earnings.

|

|

|

|

|

| |

| Inflation eating into the value of savings |

|

|

Inflation eating into the value of savings

Source: ONS, Bank of England

At the end of September, the US bank, Goldman Sachs, launched a new online easy-access savings account in the UK under the name of Marcus. It has offered a similar account in its home territory since 2016, gaining over 1.5 million customers according to the bank’s second quarter results. In the UK, 50,000 Marcus accounts were opened in the first fortnight after its introduction.

Marcus gained heavy press coverage at launch, not least because the interest rate on offer was – and at the time of writing, still is – top of the instant access league tables. The headline rate is 1.5%, but that is not quite the whole story. The rate is actually a variable 1.35%, plus a 0.15% ‘bonus’ payable for the first 12 months. However, even the 1.35% would leave Marcus very close to the top of the league tables.

|

|

|

|

|

| |

| The risks of late estate planning |

|

|

Imagine you are named as the executor and a beneficiary of your wife’s wealthy aunt. You learn that she is suffering from terminal cancer and has ‘a very impaired lifespan’. What do you do?

This is what happened in the case of Nader and others v Revenue & Customs. The executor/beneficiary, a Dr Nader, decided to consult a leading firm of accountants about inheritance tax (IHT) mitigation options for Miss Dickins (the aunt).

The accountants put forward an offshore trust-based scheme, provided by a third party, which would remove the IHT liability on £1,000,000 of Miss Dickins’ estate. The scheme was highly complex, involving multiple trusts and short-term loans. It cost a total of £100,000 in fees and its first stage was triggered on 6 December 2010, three weeks before Miss Dickins’ death.

Dr Nader received grant of probate on 4 July 2011 and a little over a month later the scheme was wound up, with IHT-free payments being made to Miss Dickins’ beneficiaries. However, subsequently HMRC opened an enquiry into the IHT return and by February 2015 – a little over four years after Miss Dickins’ demise – tax demands were issued to the beneficiaries.

|

|

|

|

|

| |

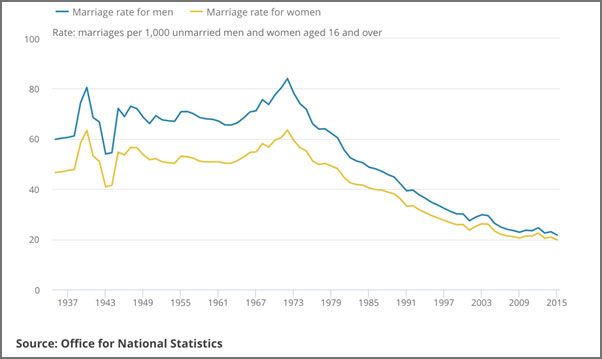

| Unmarried couples lack the rights of married couples |

|

|

Two recent events have shone different lights on the government’s view of unmarried couples.

Marriage Rates in England and Wales

As the graph shows, marriage has been drifting out of fashion for close to 50 years. There are now over 3.3 million unmarried couples in the UK, of which nearly half have children.

In spite of this major social change, governments have largely maintained sharp legislative distinctions between the married and unmarried. When they have conflated the two, it is usually to swell the Exchequer’s coffers, for example when applying the high income child benefit charge to unmarried couples with children.

|

|

|

|

|

| |

| The Budget: an end to austerity? |

|

|

The 2018 Budget – delivered on a Monday for the first time since 1962 – produced a number of surprises, not least some high-profile ‘giveaways’.

Announcements in the Budget included:

• A £650 increase in the personal allowance to £12,500 for 2019/20, the level originally pencilled in for 2020/21.

• A £3,650 increase in the higher rate threshold to £50,000, again targeted for 2020/21.

• A £25,000 increase in the pension lifetime allowance to £1,055,000 from April 2019.

• A one-third reduction in business rates on smaller retail premises, starting from next April.

• An increase in the annual investment allowance (AIA), from £200,000 to £1,000,000, from January.

However, Mr Hammond’s generosity was not all it appeared. For instance, the personal allowance and higher rate threshold will both be frozen in 2020/21, while the business rates reduction and higher AIA will only last for two years. The Chancellor also kept many tax thresholds and allowances unchanged. |

|

|

|

|

| |

| The third quarter of 2018 showed mixed results for global stock markets. |

|

|

Index |

2018 Change |

FTSE 100 |

-0.7% |

FTSE All-Share |

-0.5% |

Dow Jones Industrial |

+7.0% |

Standard & Poor’s 500 |

+9.0% |

Nikkei 225 |

+ 6.0% |

Euro Stoxx 50 (€) |

-3.0% |

Shanghai Composite |

-14.7% |

MSCI Emerging Markets (£) |

-6.2% |

In the US, shares have continued to power ahead, despite another rise in interest rates in late September and Mr Trump’s trade battles. It has been a different story in emerging markets, which have suffered from two key US factors: a strong dollar and those rising interest rates.

Japan has also performed well, with the Nikkei 225 reaching a 27-year high at the end of September. Meanwhile, Europe ended September on a down note, with worries about Italian government borrowing resurfacing just as the month closed. And for all the traumas of Brexit, the UK is marginally ahead of the rest of Europe across the first nine months of the year.

|

|

|

|

|

| |

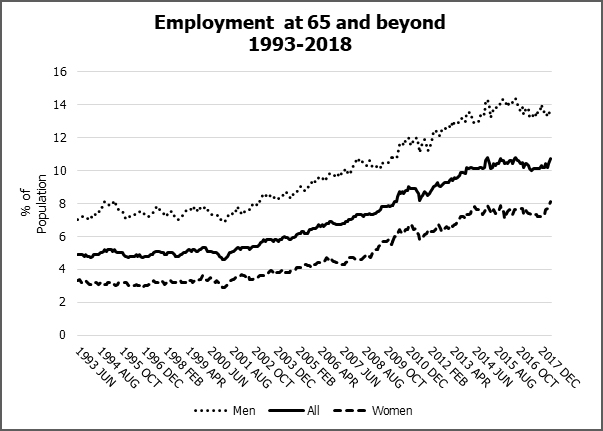

| More people working past 65 |

|

|

Do you fancy working once you have reached age 65? The trend of rising employment levels is not limited to working-age people, according to the latest employment statistics from the Office for National Statistics. A

Source: ONS 11/9/2018 B

The data reveals a growing number of people have working beyond what is still often thought of as male pension age since the start of the millennium. From May to July 2018, 10.7% of the population aged 65 or over were in employment. Women aged 65 or over are less likely to be working, but the proportion who are has increased to 8.1% from 4.7% in July 2008.

In fact, 65 will be women’s state pension age (SPA) from November 2018, but only briefly. From December 2018 the next phase of SPA increases begins, reaching a SPA of 66 for both men and women by October 2020. These increases, with yet more rises by March 2028, make it almost certain the percentages will increase further.

|

|

|

|

|

| |

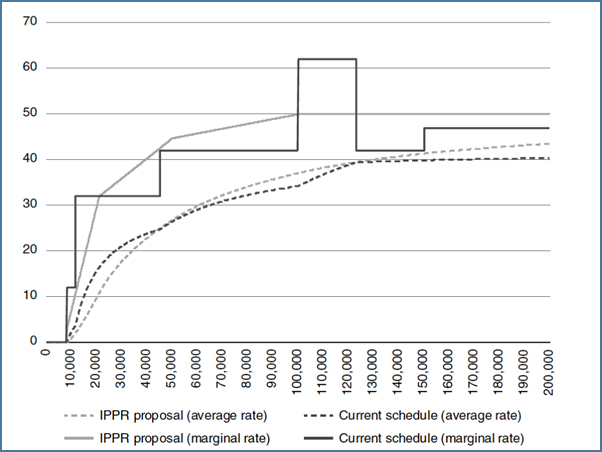

| A different view on tax reform |

|

|

A leading think tank has proposed a radical shake up of the UK tax system.

The Institute for Public Policy Research (IPPR) is a centre-left think tank that has a long history of influencing Labour Party policy. So, its ideas on tax reform published in the final report of its ‘Commission on Economic Justice’ A are of more than just academic interest.

Income tax and national insurance – The IPPR propose combining income tax and national insurance contributions (NICs) into a single tax, applicable to all income, including investment income. They would replace the current system of incremental tax bands with a gradually rising rate applied to all taxable income, capped at a maximum 50% marginal rate above £100,000. Their proposal would smooth out inconsistent marginal rates, as the graph shows.

Source: IPPR

|

|

|

|

|

| |

| Class 2 NICs here to stay |

|

|

The Chancellor has changed his mind – again – on National Insurance Contributions (NICs) for the self-employed. The Treasury has revealed that Class 2 NICs will remain for at least the rest of this Parliament.

The Treasury’s justification was that, without Class 2 NICs, “A significant number of self-employed individuals on the lowest profits would have seen the voluntary payment they make to maintain access to the state pension rise substantially.” A

This means that over three million people will continue to pay the tax, providing more revenue for the Chancellor at a time that he certainly needs it. However, as many as 300,000 self-employed people earning less than the Small Profits Threshold (£6,032 a year) could have seen their NIC payments rise from £2.95 a week to £14.65 a week. B

Mr Hammond originally proposed a reform of National Insurance Contributions (NICs) for the self-employed in his March 2017 Budget. The 2017 proposal was to increase the main rate of Class 4, from 9% to 10% in 2018/19 and again to 11% in 2019/20, bringing it closer to the employee rate of 12%.

|

|

|

|

|

| |

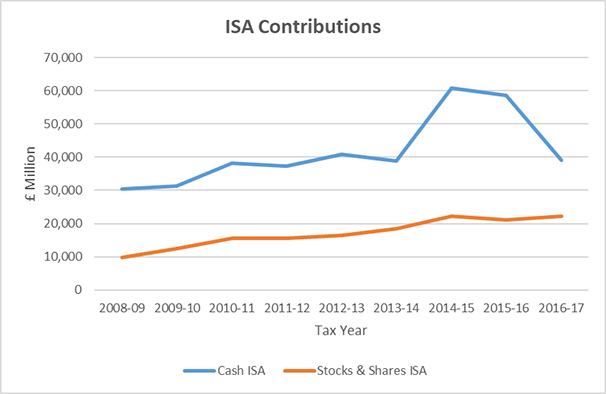

| Losing interest in cash ISAs |

|

|

The popularity of cash ISAs is continuing to wane, according to new statistics from HMRC. With inflation persistently above interest rates, it’s not hard to imagine why.

The bank of England recently increased the interest rate to 0.75%, A but inflation was 2.7% B in August 2018. This means, if you are holding cash in an ISA or considering topping up an existing account, you need ask yourself two questions:

1. What interest rate are you earning? You could be earning less than the current 0.75% base rate, particularly if the account is not open to new investors.

2. Do you need a cash ISA at all? The personal savings allowance means you can earn interest of £1,000 tax-free per tax year if you are a basic rate taxpayer, or £500 if you pay tax at the higher rate.

For a variety of reasons, not least cheap funding available from the Bank of England, competition in the cash ISA market has waned. For example, the Halifax is offering only 0.6% to new ISA investors for 12 months (and just 0.2% thereafter – the rate for existing Instant ISA Saver investors). C Also, last month National Savings & Investments cut the rate on its Direct ISA to 0.75%, defying August’s increase in the Bank of England base rate.

|

|

|

|

|

| |

| Trick or treat? The Chancellor calls the 2018 Budget for late October |

|

|

The 2018 Budget has been set for Monday 29 October, setting a deadline for speculation and proposals. Mr Hammond, however, has indicated that he won’t end the long spell of austerity measures, despite improving public finances.

Proposals raised by think tanks and professional bodies include overhauls of income and inheritance tax, ‘pension tax relief simplification’, and scrapping entrepreneur’s relief to help fund NHS costs.

But every proposal is overshadowed by Brexit, and the uncertainty of what will happen on 29 March 2019.

What’s coming?

Alongside measures announced in the draft Finance Bill, the following areas could see change:

The NHS – The NHS Foundations’s ten-year plan may not be published in time for the Budget, so the Chancellor could be limited to general spending priorities. Mr Hammond said a digital services tax or ‘Google tax’ is coming – with or without European allies. This income could be dedicated to the NHS.

Inheritance tax (IHT) – The IHT review from the Office of Tax Simplification (OTS) may be published ahead of the Budget. It was tasked to look at making IHT less complex, focusing especially on trusts, administrative issues and business and agricultural property reliefs. Calls for a complete overhaul in favour of a ‘lifetime receipts’, ‘property’ or ‘wealth tax’ seem unlikely from a Conservative government.

Stamp duty – After introducing new reliefs for first-time buyers, focus has shifted to ‘last time’ buyers, with calls to incentivise older homeowners to downsize. The Prime Minister has also indicated that an additional 1-3% duty could be levied on foreign property buyers to help control rising house prices and tackle homelessness.

|

|

|

|

|

| |

| The record S&P 500 bull run |

|

|

The US stock market set a new record for the longest-ever bull market in August.

S&P 500 Index Performance

Wednesday 22 August 2019 saw the S&P 500 drop – by less than 0.1% – after 3,453 days, making it the longest-ever bull run (a period of rising share prices) for the index, which is used by professional investors’ as a yardstick for the US stock market.

The previous record was set between 1990 and 2000, a period that saw the dot-com boom, followed shortly after the start of the new millennium by the tech bust.

The current rally has been helped by a strong performance from technology stocks, notably the ‘FAANGs’ (Facebook, Apple, Amazon, Netflix and Google (now called Alphabet)). It has also been aided by a period of ultra-low interest – the US Federal Reserve’s main rate was set to a historic low in December 2008 and did not rise above 1% until June 2017. In the last year US companies have also benefitted from Donald Trump’s corporate tax cuts, which have boosted earnings figures.

|

|

|

|

|

| |

| Student loan interest rates increase |

|

|

The rates charged on student loans rose at the start of September.

The revised terms for interest on, and repayment of, student loans were published in August, along with the A level results for the year. From 1 September, the main interest rates for Plan 2 loans, taken out by students and recent graduates in England and Wales, are:

Period |

Interest Rate |

During study and until the April after leaving the course. |

6.3% |

From the April after leaving the course (maximum 30 years). |

On a sliding scale, rising from:

3.3%, where income is £25,725 or less; up to

6.3%, where income is £46,305 or more. |

Plan 1 student loans, taken out by students in Scotland and Northern Ireland (and students in England and Wales whose course started before 1 September 2012), carry a 1.75% interest rate.

Both rates represent an increase – 0.2% for Plan 2 and 0.25% for Plan 1. The first was driven by an increase in the RPI for March 2018 against March 2017, and the second by last month’s base rate rise.

The income threshold at which loan repayments start to be made will also rise from 6 April 2019, to £25,725 for Plan 2 RPI-linked loans and £18,935 for the older Plan 1 loans. The repayment level will be held at 9% of the excess income, meaning the cheaper loans will require higher repayments.

|

|

|

|

|

| |

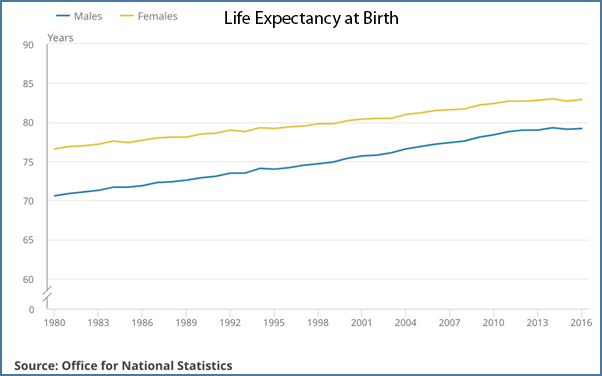

| Slowing down our old age |

|

|

A paper published in August by the Office for National Statistics (ONS) casts new light on life expectancies in the UK.

Life expectancy has been increasing in the UK for a long time, as the graph shows. In 1980, the average life expectancy at birth was 70.6 years for a man and 76.6 years for a woman. In 2016 this had increased to 79.2 years for a man and 82.9 years for a woman.

What the graph also reveals is that the rate of improvement in life expectancy has been slowing down. The ONS data shows a marked deceleration in the 21st century.

Between 2011 to 2016, women’s life expectancy at birth increased by 0.2 years compared with an increase of 1.2 years over the period from 2006 to 2011. For men, the corresponding increases were 0.4 years and 1.6 years. There was a similar effect for life expectancy at age 65, which rose by only 0.1 years for women and 0.3 years for men between 2011 and 2016, against 1 year and 1.1 years in the previous five years.

For the layman, this welter of data can be confusing, especially as the press coverage is not always well informed. A few important things to understand are:

The ONS life expectancy data imply that, on average, a man who was 65 years old in 2012 will live until 83.7, while a woman who was 65 years old in 2012 will survive until 86. The expected age at death also rises with age attained.

|

|

|

|

|

| |

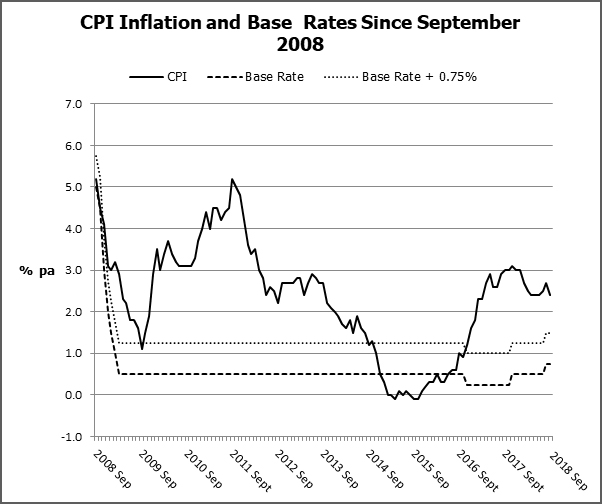

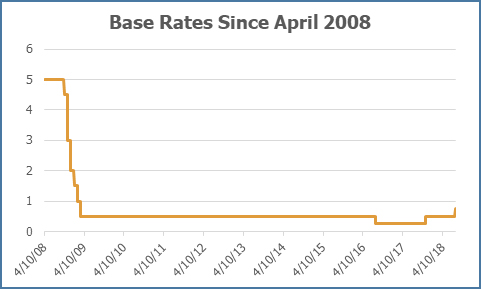

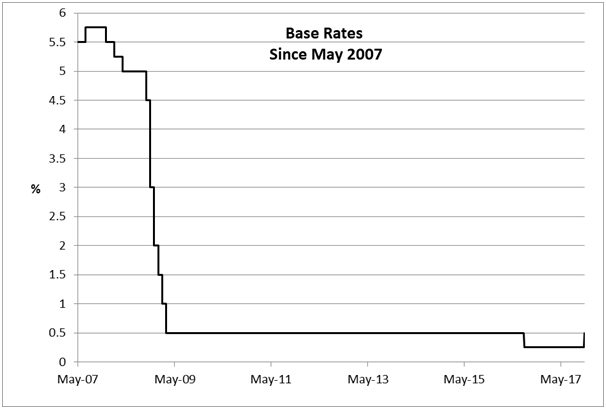

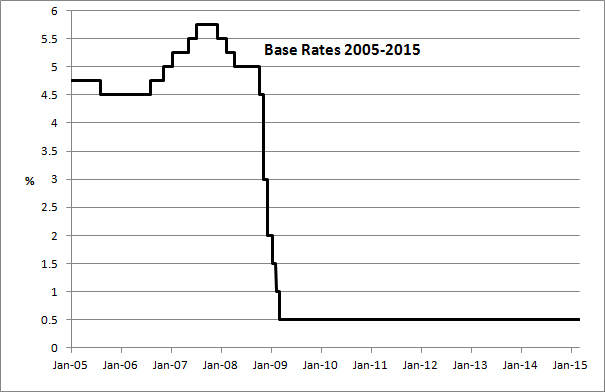

| Interest rates creeping up after nine years |

|

|

The Bank of England increased the base interest rate in August to 0.75% – the second increase in 12 months.

Source: Bank of England August 2018

The Bank’s decision to raise the rate to its highest level in nearly nine and a half years was no great surprise to the investment community. Of more interest to the experts were the comments the Bank offered on the long-term trend of base rates relative to inflation. The Bank gave a theoretical estimate of the base rate needed to maintain inflation and economic growth in a fully functioning economy, rather than another forecast of where rates might be in a year’s time.

The Bank said an interest rate of 0%–1% above the rate of inflation, with a ‘modal rate’ of 0.25%, would achieve this equilibrium. In today’s economic environment, with an inflation target of 2%, this would mean a base rate of around 2.25%. That implies:

The equilibrium rate will be a long time coming – several 0.25% increases would be required and the Bank has repeatedly said any changes will be gradual.

|

|

|

|

|

| |

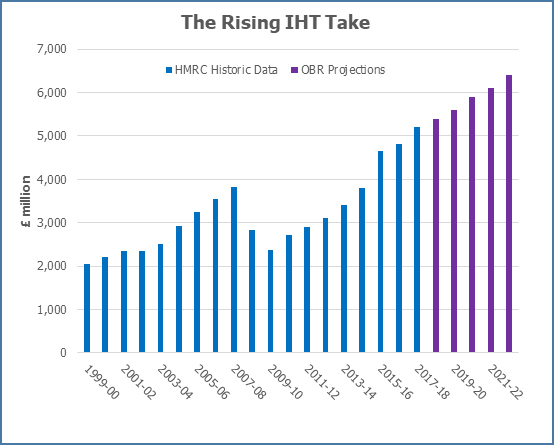

| Record inheritance tax revenues ahead of simplification review |

|

|

2017/18 produced record inheritance tax (IHT) receipts according to HMRC data published in July.

The latest release of the annual statistics revealed IHT produced £5.228 billion for the Exchequer in 2017/18, an increase of two thirds over just five years. As the graph shows, IHT revenue has been rising rapidly since Treasury receipts hit a low in 2009/10, owing to the impacts of the financial crisis and the introduction of the transferable nil rate band.

The Office for Budget Responsibility (OBR) expects the growth to continue, although the rate of increase will slow for the next few years because of the introduction from April 2017 of the residence nil rate band.

|

|

|

|

|

| |

| Is the LISA’s short life about to end? |

|

|

The Lifetime ISA (LISA) may not survive after low uptake by providers and fresh criticisms from parliament.

The LISA has been reviewed by the Treasury Select Committee, which was critical of, “its complexity, its perverse incentives, its lack of complementarity with the pension saving landscape and its apparent lack of popularity with the industry and pension savers”. The Committee concluded by recommending “The Government should abolish it.”

The LISA was announced by the previous Chancellor, George Osborne, in his final Budget in Spring 2016. It was intended to appeal to savers under 40 by combining a first-time buyer’s deposit saving scheme and a pension arrangement, stretching the ISA idea into a very new shape.

Despite reservations from the Financial Conduct Authority about the regulatory implications, and reluctance from the savings industry, Philip Hammond launched the LISA in April 2017. Progress has been limited since then as there is still only one provider of cash LISAs. There is a wider choice of stocks and shares LISAs, but these are generally not suitable as deposit saving arrangements.

|

|

|

|

|

| |

| OBR forecasts present need for tax increases in the Budget |

|

|

The long-term outlook for government finances suggests tax increases are inevitable.

The Office for Budget Responsibility (OBR) produces medium-term financial forecasts alongside the Budget and Spring Statement, but that is not its only task. It is also required to take a longer-term view of the public finances, producing a Fiscal Sustainability Report every two years.

The latest version of the report was published in mid-July and did not make for comforting reading. The graph is a good summary of the bad news:

• The black lines show the projected government borrowing as a percentage of the size of the UK economy. In 2017/18 annual borrowing was 1.9% of Gross Domestic Product (GDP). By 2067/68 it becomes 85.6%.

• The red line shows the total amount of government debt, also as a proportion of the UK economy. As at May 2018, total borrowing was 85.0% of Gross Domestic Product (GDP). By 2067/68 it becomes 282.8%.

In the report, the OBR says, “Needless to say, in practice policy would need to change long before [2067/68] to prevent this outcome.” That means reduce expenditure and/or increased taxation.

|

|

|

|

|

| |

| Residential letting to get more difficult |

|

|

Draft legislation released in July contains more bad news for those renting out residential property.

The Finance Bill 2018/19 draft legislation published just before the summer holidays has confirmed the following measures:

• From 6 April 2019, the rules for rent-a-room relief (which exempts up to £7,500 a year of income from tax) will be revised. A new ‘shared occupancy test’ means the relief will no longer apply if the entire property is rented out for the tenancy period. This will mean an end to going on holiday and letting out your home tax-free during sporting events, such as Wimbledon.

• From 1 March 2019, the window for filing and paying stamp duty in England will shrink to just 14 days from the date of sale. Past experience suggests Scotland and Wales will follow suit.

• From 6 April 2020, for residential property sales giving rise to taxable gains, a tax return must be made and the capital gains tax (CGT) paid within 30 days of the sale. Any adjustments would then need to be made via a self-assessment return.

Over the past few years, the Treasury has turned its attention to the private rented sector. As such, landlords must already comply with several new rules, including: the wear-and-tear allowance for furnished lettings being replaced with a tighter expenditure-based regime; the phased replacement of full income tax relief on finance interest costs with a basic rate tax credit; a 3% stamp duty surcharge for second residential properties; and an 8% capital gains tax surcharge on residential property.

|

|

|

|

|

| |

| 2018 proves volatile after the smooth sailing of 2017 |

|

|

The first six months of 2018 were unpredictable times for investors as global stock markets suffered a sudden bout of volatility.

Source: LSE

The unpredictability came as a major surprise after the general stability of 2017. Once the dust had settled there was a mixture of good and bad news.

The UK markets were inevitably led by Brexit, with negotiations mainly at the intra- rather than inter-government level. The other perennial British topic, the weather, produced the Beast from the East, depressing economic activity in the first quarter.

|

|

|

|

|

| |

| Is a flat rate scheme coming to pension tax relief? |

|

|

The prospect of a flat rate of tax relief on pension contributions has resurfaced in the national press.

The cost of pension relief has been chipped back in recent years, mainly by reducing the annual allowance. However, a report in The Times in early July suggested the Treasury is looking at flat rate tax relief, which would give the same rate of tax relief on contributions, regardless of personal income tax rates. The Times reported a flat rate of 25% is being considered, meaning a gross pension contribution of £100 would require a net outlay of £75 instead if the current £80.

The 25% rate would be an effective tax cut for the majority of pension contributors, who pay basic rate tax, but would potentially save the Exchequer about £4 billion a year. It is estimated that a flat rate of 28% would cost the Treasury the same as today’s mix of 20%, 40% and 45% reliefs.

It is hardly surprising that the Treasury is re-examining pension tax relief, given it is looking for an extra £20.5 billion for NHS funding. Tax relief on pension contributions cost the Exchequer £38.6 billion in 2016/17 according to HMRC’s latest estimate, as well as over £16.2 billion of national insurance contribution (NIC) relief on employer contributions.

It remains to be seen if such a change will be announced in the Budget. Currently, the politics of such a move seem between difficult and impossible, and the Chancellor will remember the backlash he faced when he attempted to raise NICs. A proposal to end higher rate tax relief could meet with similar resistance, especially as it would likely coincide with the next rise in automatic enrolment pension contributions. However, a recent Treasury Select Committee report recommended the Government give “serious consideration” to the introduction of flat rate relief.

|

|

|

|

|

| |

| Saudi Arabia: the next emerging market |

|

|

The June 2018 review of constituents for the main Emerging Markets Index has produced a few surprises.

The MSCI Emerging Markets Index is one of the most important global stock market indices. JP Morgan, the US investment bank, estimates that nearly $1,500 billion is either benchmarked against the index or directly tracks it, so there can be considerable implications for stock markets if the constituent countries of the Index change.

Last year’s MSCI review saw Chinese mainland shares promoted to the Index, with that process now starting to take effect.

The 2018 review heralds two potential new arrivals in the MSCI Emerging Markets from May 2019:

• Saudi Arabia should join the Index in a two-stage process (as is now happening with China). The first stage follows the May 2019 half-yearly index review, and the second as part of the August 2019 quarterly review.

Saudi Arabia will initially account for 2.6% of the Index, but it could become more important when Saudi Aramco, the state oil company, is partially floated, probably next year.

• Argentina is set to return to the Index, having been demoted to ‘Frontier Market’ status in 2009. Ironically, the MSCI announcement almost exactly coincided with confirmation that that IMF had agreed $50 billion of stand-by credit for the country.

At present Argentina represents almost a fifth of MSCI's Frontier Markets Index, so if it does move across, there will be a significant rebalancing of that index.

|

|

|

|

|

| |

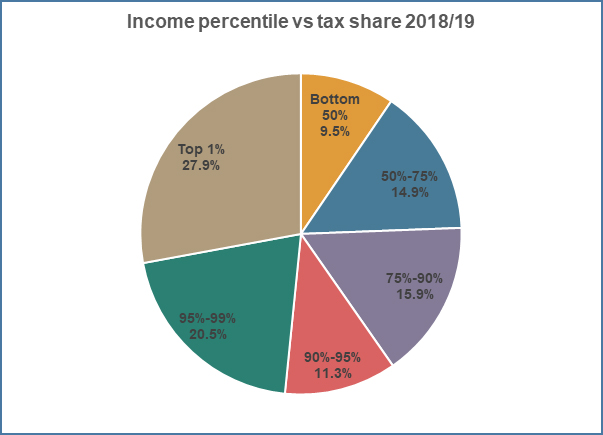

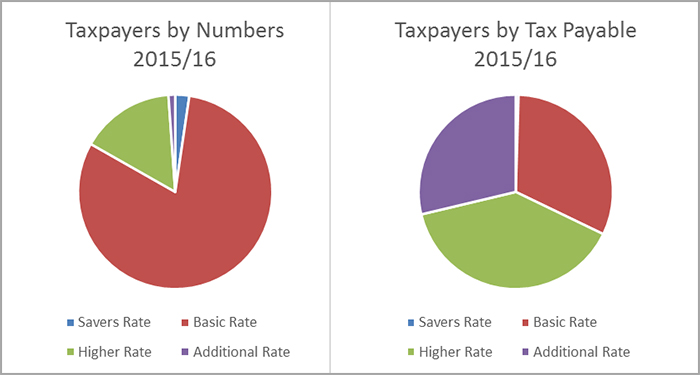

| Top earners increase their share of tax payments |

|

|

HMRC’s latest statistics provide an insight into the income tax paying population.

The figures reveal changes in the distribution of tax revenue over the last decade, with a growing share now coming from higher earners.

The pie chart shows the proportion of 2018/19 tax expected to be paid by taxpayers in various bands of income. For example, the smallest wedge shows that the bottom 50% of income tax payers (those with annual income of up to £25,500) will provide 9.5% of all income tax receipts.

At the opposite end of the scale, the largest wedge is the top 1% (with incomes of at least £177,000) who will supply 27.9% of the £185 billion of income tax the Treasury hopes to receive for the current tax year. In other words, over a quarter of income tax comes from ‘the 1%’.

The Exchequer’s dependence on a small group of wealthy taxpayers is nothing new. However, the concentration has grown since the start of the decade. For example, in 2010/11 – when additional rate tax first appeared at the 50% rate – the contribution from the top 1% was 25.0%. For the top 10% of taxpayers (with income of at least £57,500 in 2018/19), the tax share has risen from 53.5% in 2010/11 to 59.7% this tax year. Over the same period the bottom 50% have seen their share drop from 11.3% to 9.5%.

|

|

|

|

|

| |

| Understanding what goes in to the FTSE100 |

|

|

The latest quarterly review of the FTSE 100 revealed common misunderstandings about how the index is drawn up.

Every quarter FTSE Russell, which operates all the FTSE indices, decides which companies are promoted or demoted from the FTSE 100 index.

There had been speculation that the June review would see Marks & Spencer (M&S) replaced by Ocado. The high street chain has been a member of the Footsie since the index first appeared in 1984, so for the bricks and mortar shopping experience to be supplanted by an online-only retailer that did not arrive on the stock market until 2010 made for a good headline.

However, M&S did not check out of the FTSE100 and survives until the next quarterly review. What the journalists missed is that a company listed in the FTSE 100 is only ejected if its ranking drops below 110. Similarly, promotion into the FTSE100 requires a ranking of 90 or higher.

These rules are designed to avoid a large quarterly churn at the bottom tier of the index, and it works – only one other company, GVC Holdings, entered the index in June.

|

|

|

|

|

| |

| National Savings & Investments focusing on smaller investors |

|

|

National Savings & Investments (NS&I) has introduced limits on its offerings for wealthier savers.

In mid-June NS&I announced a revision to the terms of its popular Guaranteed Growth and Guaranteed Income Bonds. The interest rates were left unchanged, but the maximum investment per person, per issue was cut by 99%, from £1 million to £10,000.

NS&I ostensibly exists to help small savers, but in recent years it has raised investment limits – for example to £50,000 on premiums bonds – to meet the funding levels set by the government. In the past NS&I has also emphasised tax-free savings certificates, which were of most appeal to top rate taxpayers.

Fortunately for existing investors, their former investment limits will continue to apply if they reinvest. The dramatic reduction means that NS&I will no longer offer an easy solution for anyone seeking fixed rates on large sums of capital without having to worry about the £85,000 FSCS deposit protection ceiling.

Fortunately for existing investors, their former investment limits will continue to apply if they reinvest. The dramatic reduction means that NS&I will no longer offer an easy solution for anyone seeking fixed rates on large sums of capital without having to worry about the £85,000 FSCS deposit protection ceiling.

|

|

|

|

|

| |

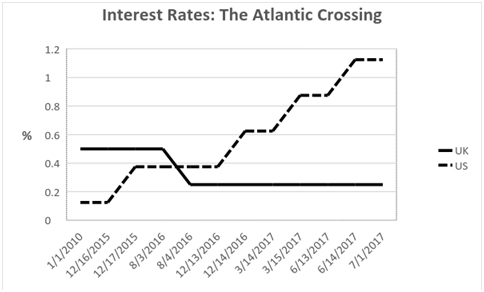

| Interest rates for the Eurozone and US diverge |

|

|

Important interest rate announcements were made in June, both in the UK and the US.

The US Federal Reserve announced its seventh 0.25% increase in interest rates since December 2015, taking the level to 1.75%-2.00%. The rise had already been incorporated in market prices by the time it arrived, so of more interest were the press release and other papers which accompanied the announcement. These pointed to two more rate rises in 2018, and possibly three more in 2019. They also dropped a long-standing reference to interest rates remaining, “below levels that are expected to prevail in the longer run”.

The following day the European Central Bank (ECB) decided to leave rates unchanged, again a widely anticipated move – the ECB has kept its main interest rate at zero since March 2016.

The market again focused on the background papers, which revealed the ECB’s tapering of its quantitative easing (QE – so-called money printing) programme, will come to an end in December and that interest rates were expected to be unchanged, “at least through the summer of 2019”. The first part was no surprise, but the statement on interest rates was not expected. The markets reacted accordingly, pushing the Euro down against the US dollar.

Controlling market shocks

The relationship between central banks and investment markets is a curious one these days as the banks go out of their way to make sure markets are kept informed. As a result, the markets are now more interested in the next-but one action. The market responses to these recent rate announcements are two good examples.

|

|

|

|

|

| |

| A savings tax review |

|

|

The way savings are taxed is being reviewed by the Office of Tax Simplification (OTS).

The OTS is looking at the way in which savings and investment income is taxed, which can be very complicated. According to its paper, published in May 2018, “the interactions between the [tax] rates and allowances is sufficiently complex at the margins that HMRC’s self-assessment computer software has sometimes failed to get it right”.

The complex marginal rules mean that, “many taxpayers continue to worry about the tax treatment of their savings income even when they do not in fact have anything further to pay, and there are also many specific complexities which taxpayers find difficult and confusing”.

To make matters worse, the OTS also found that 95% of people do not pay tax on savings income, thanks to a combination of the personal savings allowance (£1,000 for basic rate taxpayers and £500 for higher rate taxpayers) and the dividend allowance (£2,000).

|

|

|

|

|

| |

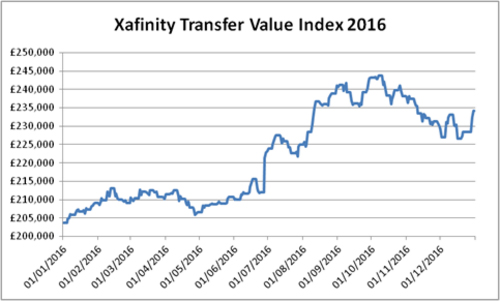

| Pension transfers skyrocket |

|

|

Transfers out of private sector final salaries boomed in 2017.

There was a dramatic increase in the value of number of transfers out of defined benefit (usually final salary) pension schemes in 2017. A recent Freedom of Information (FoI) request to the Financial Conduct Authority (FCA) revealed that the £20,800 million was transferred last year, up from £7,900 million in 2016. There were 92,000 transfers, compared to 61,000 in 2016.

The increase in transfers stems from a variety of factors:

• A growing awareness of the planning opportunities introduced by pension flexibilities, which can make the traditional defined benefit scheme look outdated and rigid.

• The significant sums involved: the average transfer last year amounted to £226,000.

• Employers quietly welcoming transfers as a way of reducing their pension scheme liabilities, which have grown rapidly because of ultra-low interest rates and improving pensioner lifespans.

• The proportion of defined benefit schemes closing to existing employees steadily increasing, leaving more people with preserved pension benefits, even if they have not changed jobs.

• Since 2009, investment markets being generally benign or buoyant, helped by the same economic measures that have pushed, and held, down interest rates. The absence of any major market declines has reduced the visibility of one of the major transfer risks: exchanging a quasi-guaranteed benefit for one reliant on investment performance.

|

|

|

|

|

| |

| Mainland Chinese stocks join the MSCI index |

|

|

Important changes affecting Chinese market indices took effect in June 2018, which could affect emerging market funds.

On 1 June 2018, the index provider MSCI added 233 domestic Chinese stocks to its emerging market and global indices. MSCI has some of the most widely used indices for measuring the performance of emerging markets, with the MSCI Emerging Market index suite providing benchmarks for over $1,900 billion of assets. This popularity means that markets can move when any revisions are made to MSCI indexes.

Previously, MSCI’s indices had only included Chinese companies with share listings outside the Chinese mainland, e.g. in Hong Kong. Although the Chinese mainland stock market is the second largest in the world, MSCI previously considered the market to have too many drawbacks to merit inclusion. The Chinese authorities have worked on the issues that concerned MSCI, such as ownership restrictions and limited liquidity, resulting in MSCI’s change of heart.

The inclusion of the 233 Chinese shares will have little initial impact on the MSCI Emerging Market Index as their total weighting will be less than 1%. However, this is likely to grow as MSCI continues to monitor the market, include more Chinese companies and reweight its indices. In theory China could ultimately represent 40% of the Emerging Markets index.

|

|

|

|

|

| |

| Interest rate rises prove hard to predict |

|

|

The Bank of England did not raise interest rates in May, despite earlier suggestions that it would.

About four years ago a member of the Treasury Select Committee compared Mark Carney, the Governor of the Bank of England, to “an unreliable boyfriend”. The remark was prompted by Mr Carney’s record of talking about future interest rates increases that never became reality. The epithet came back to haunt the Governor last month.

The Bank had been hinting strongly that rates would rise in May, and by early April the money markets were effectively putting the odds on a May increase at 90%. However, a combination of surprisingly bad economic numbers – growth fell to just 0.1% in the first quarter – and downbeat business surveys prompted a rethink. By the time the Bank announced the rate would be held at 0.5% on 10 May, nobody was surprised.

The next opportunity for changes to the interest rate will come on 2 August 2018, when the Bank publishes its next Quarterly Inflation Report. The medium-term expectation is still that interest rates will rise, unless something disastrous happens to the UK economy. For its part, in May the Bank repeated its familiar mantra that, “any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent”.

If you have investments in fixed interest funds, now could be a good time to review those holdings. As the graph shows, the yield on 10-year government bonds is already around double the low hit in the wake of the Brexit vote. It could rise further – depressing bond prices – if the Governor becomes more reliable in his rate rise forecasts.

|

|

|

|

|

| |

| Can a revised tax system re-balance intergenerational fairness? |

|

|

A new report has proposed taxing the baby boomers to help resolve major issues around intergenerational fairness.

The report, published by the Intergenerational Commission in May, offers ten policy recommendations which would represent a radical overhaul of the UK tax system.

Examples include replacing inheritance tax with “a lifetime receipts tax that is levied on recipients with fewer exemptions, a lower tax-free allowance (£125,000) and lower tax rates (20% and 30%)”, and replacing council tax with a “progressive property tax” levied on owners rather than occupants, with a marginal rate of 1.7% on property value over £600,000.

The Commission was set up by the Resolution Foundation to examine the issue of fairness between the generations, and has been examining whether the baby boomer generation (1946-1965) has left generation X (1966-1980) and the millennials (1981-2000) to pick up the bill.

Their report found the post-war generation has the advantage, based on a range of measures including home ownership, earnings progression, personal debt and pension wealth.

As with most think tank reports, this grand plan is unlikely to be put in place. However, some of the proposals could see the light of day, as ministers look for solutions to the problem.

|

|

|

|

|

| |

| Taking early advice on your tax return |

|

|

HMRC is starting the tax year with their annual reminder to submit your tax return.

HMRC’s reminder might seem early, but its statistics show that 750,000 people (6.5%) missed the deadline for 2016/17, potentially facing an immediate £100 penalty, even if they had no outstanding tax to pay. Anyone with a 2016/17 return still outstanding could also be clocking up additional penalties of up to £10 per day.

HMRC cancelled more than a third of all the penalties initially levied in 2014 and 2015 according to statistics obtained under a Freedom of Information Request. However, it is best not to incur the fine in the first instance, even if you have what HMRC calls a ‘reasonable excuse’.

You have until the end of October 2018 to submit a paper tax return and 31 January 2019 if you file your return online. According to HMRC, 9.92 million out of 11.43 million tax returns for 2016/17 were filed online by 31 January 2018, while 0.77 million were made on paper.

|

|

|

|

|

| |

| Repayment threshold increases for student debt |

|

|

The income threshold at which student loan repayments begin rose on 6 April 2018.

English and Welsh students who started their courses after 31 August 2012 can now earn £25,000 a year – up from £21,000 – before they have to start repaying their student loans. The increase could provide a saving of £360 a year, with repayment rates at 9%.

Although the change was heralded as good news, that is not the whole story:

• Automatic enrolment pension contributions nearly tripled at the same time. For those earning £29,000 or more, this increase more than wipes out the savings from the repayment threshold increase.

• Interest rates for student loans have not changed. Before graduation, interest remains at RPI + 3% (currently 6.1%, and 6.3% from September 2018). After graduation interest is charged at RPI for those earning up to £25,000, rising on a sliding scale up to RPI + 3% for those earning £45,000 or more.

• As with any loan, lower repayment levels mean a longer payment period. Although student loans are capped at 30 years, after which the debt is written off.

• The Institute for Fiscal Studies estimates that the higher threshold will cost the taxpayer £2.3 billion a year, and that the government will end up writing off about 45% of total student debt.

|

|

|

|

|

| |

| How useful is the Dow? |

|

|

The Dow Jones industrial Average – the Dow – is a well-known part of the investment market, often quoted by news sources. But what does it mean, and is it useful when making investment decisions?

The Dow was created in 1896, and is arguably still used today mainly thanks to history or habit.

There are several issues with the Dow, such as:

• The index only tracks 30 shares.

• It has a large absolute value – around 25,000 – which means movements sound bigger than they are. ‘Dow falls 500 points’ has more impact than, ‘Dow falls 2%’, even if the two measures are identical.

• A committee chooses which shares the Dow tracks – where most main indices choose their constituents by market capitalisation – so it has some surprising absences, such as Alphabet (Google’s holding company) and Facebook.

• Almost uniquely, the Dow is weighted by share price rather than company stock market value, which has some strange effects. Because a high share price means a larger weighting, Boeing (with a share price around $320) has nearly double the weight of Apple (with a share price around $170), even though Apple is the largest US company and over four times the size of Boeing.

When China recently announced proposed tariffs on imported aircraft aimed at Boeing, this had a disproportionate effect on the Dow, as Boeing shares (over 9% of the Index) fell.

|

|

|

|

|

| |

| Increasing inheritance benefits for couples |

|

|

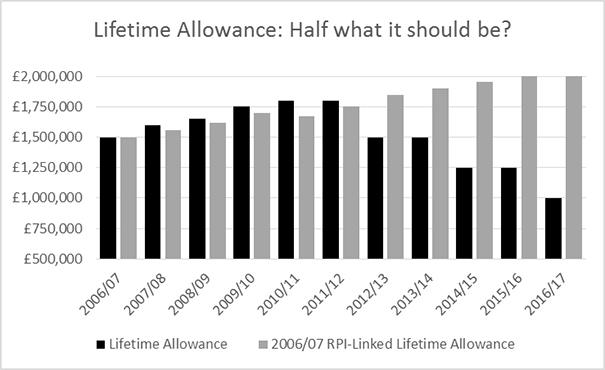

Couples could now save an extra £20,000 of inheritance tax (IHT), as the residence nil rate band (RNRB) increased in April 2018.

The RNRB was increased at start of the new tax year and it is due to increase by £25,000 in each of the next two years, reaching £175,000 in 2020/21. It will be indexed to the Consumer Price Index after that.

The RNRB was introduced to give married couples and civil partners an eventual total IHT exemption of £1 million. This new band was introduced rather than increasing the existing nil rate band, which has been at £325,000 since 2009.

Whilst the increase is good news, the RNRB creates a lot of complexity for the taxpayer. A good example is that the £125,000 band is reduced by £1 for each £2 of estate over £2 million. So, in 2018/19 your RNRB is lost completely if your estate exceeds £2.25 million.

However, the estate value is calculated at death, so if gifts are made only days before death to reduce the estate below the £2 million threshold, the RNRB is not lost – a potential tax saving of up to £50,000 at present. A surviving spouse or civil partner can also double that saving by inheriting any unused RNRB from their partner.

|

|

|

|

|

| |

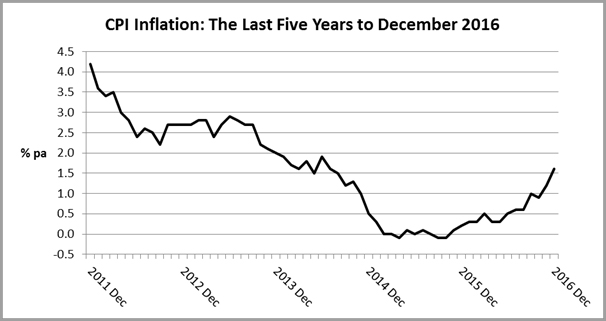

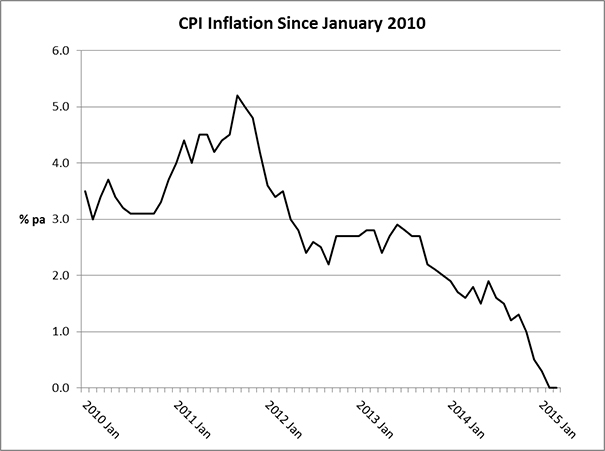

| The pressure is dropping on inflation |

|

|

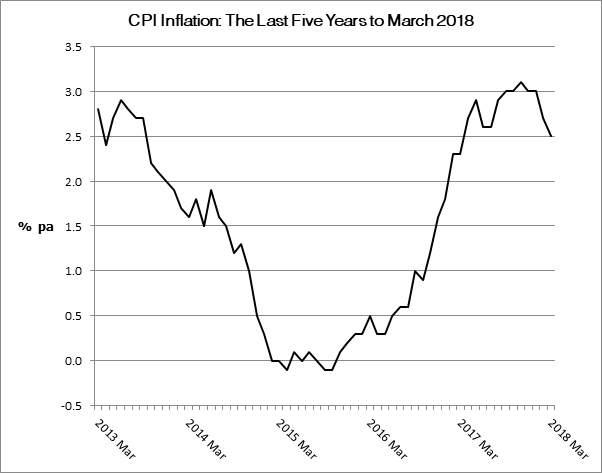

UK inflation is falling faster than expected, as the March figure for the Consumer Price Index (CPI) was 2.5%.

This March figure, published in mid-April, surprised forecasters, who had predicted annual inflation would remain at 2.7%, as in February. That February figure was itself a surprise, as the forecasts had predicted 2.8%.

The drop for March may be the result of one-off factors, so it should be treated with caution. One issue is the way individual categories can distort the final figure. In March, alcoholic drinks and tobacco saw the sharpest drop price – from 5.8% to 3.5%. These both saw two sets of tax increases in 2017, because of the double Budgets, whereas in 2018, the Chancellor moved to a Spring Statement and did not change any taxes. It was the classic one-off.

|

|

|

|

|

| |

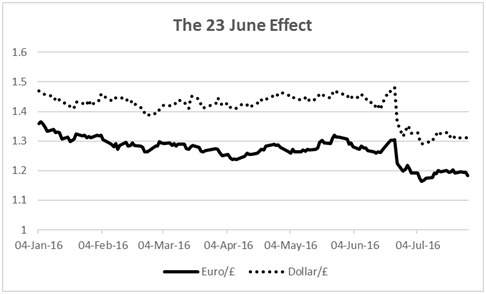

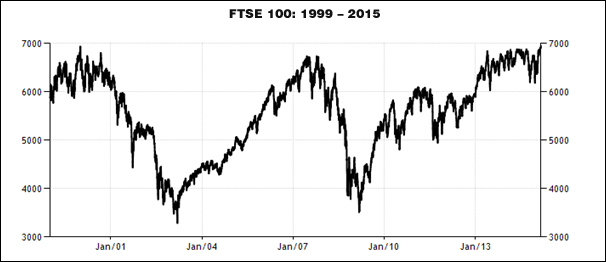

| International investments and Brexit |

|

|

With Brexit now less than a year away, how insular are your investments?

Brexit – or more accurately the start of the transition/implementation period of the UK leaving the EU – begins on 29 March 2019. By the end of the following year, the UK’s remaining links to the EU are due to be cut.

Since June 2016, when the Brexit referendum took place, the FTSE 100 has been one of the world’s poorest performing major indices. So it is perhaps no coincidence that, in March 2018, a survey by the Bank of America (BoA) of 163 global investment managers found the UK stock market was least popular of 22 wide-ranging investment asset classes.

If you live and work in the UK, then naturally enough you tend to think in terms of UK-based investments, be they shares, bonds or property. The BoA survey is a reminder that taking such a parochial view of investments may come at a price.

Diversification is one way investment professionals limit risk and potentially increase returns. For example, the most recent report from the Pensions Regulator showed that in 2017 the average UK defined benefit pension scheme had only one fifth of its total shareholdings in UK quoted shares.

|

|

|

|

|

| |

| What does the pension lifetime allowance buy? |

|

|

It is worth looking at what your pension pot could buy for your retirement.

The importance of pension contributions has been bolstered by the rollout of auto-enrolment pension schemes. However, it is not as clear what your savings will give you when you come to retire.

For example, Louise, a healthy, non-smoking 65-year-old, reaches retirement with £1,000,000 in her pension plan. If she uses the entire fund to buy herself an inflation-proofed income, what will be her first monthly pension payment before tax is deducted?

A. £2,500

B. £3,000

C. £3,500

D. £4,000

The answer is A, based on current pension annuity rates. After tax, if Louise has no other income, her monthly payment will be about £2,200. Include a 2/3 widow’s pension and the gross amount drops by about £400 a month (roughly £320 after tax).

This may be a surprise as the National Living Wage is nearly £1,200 a month for a 35-hour week. Especially when you remember Louise forgoes a tax-free lump sum of up to £250,000 in favour of a higher income.

The income of £2,500 a month (£30,000 a year) is only 3% of the pension pot, but it is RPI-linked. Importantly, because it is an annuity payment, it is also guaranteed throughout life – however long that may be.

|

|

|

|

|

| |

| Taking the early view on ISAs |

|

|

There are advantages to planning your ISA investments around the start of the tax year.

With ISAs all the taxation benefits occur after investment is made, yet the focus is often on year-end contributions. Various articles on ISAs filled the weekend press in March, and are set to re-emerge like a financial sign of spring in 12 months’ time.

For other investments, such as venture capital trusts and pensions, there is a logic in waiting until the end of the tax year – you have a better idea of your income for the year and hence your tax position. The same is not necessarily true of ISAs.

Indeed, it is sensible to contribute to ISAs as early in the tax year as possible, to get the tax benefits for as long a period as possible. As a reminder these are:

• No UK tax on dividends, an important factor as the dividend allowance has been cut from £5,000 to £2,000 for 2018/19.

• No UK tax on interest earned.

• No UK capital gains tax on any profits realised.

• Nothing to report to HMRC on your tax return.

• Allowing a surviving spouse or civil partner to inherit your ISA benefits, effectively treating your ISAs as joint investments.

Making an ISA contribution does not necessarily mean paying in cash. It can include selling an existing investment you hold personally and repurchasing it within an ISA. You may crystallise some capital gains in the process, but at the start of the tax year you almost certainly still have your full £11,700 annual exemption available.

|

|

|

|

|

| |

| New risk criteria for venture capital schemes |

|

|

Important changes for venture capital schemes and enterprise investment have recently come into effect.

New ‘risk-to-capital’ conditions apply to investments in venture capital trusts (VCTs), enterprise investment schemes (EISs) and seed enterprise investment schemes (SEISs). The changes took effect on 15 March 2018, when the Finance Act 2018 received Royal Assent.

Broadly speaking, an EIS or SEIS company, or a company in which a VCT is investing must both:

1. Have objectives “to grow and develop its trade in the long term”.

2. Carry a “significant risk that there will be a loss of capital of an amount greater than the net investment return”.

The changes are intended to end venture capital schemes – particularly EISs – which often did little more than return the investor’s original capital at the end of the tax relief clawback period. Such schemes were usually asset-backed, typically focusing on pubs, ship ownership/chartering or film production, where pre-sales were in place.

For many years the Treasury tried to exclude such ‘safe’ trades, only for other low-risk options to emerge. The new risk-to-capital condition, and its somewhat subjective criteria, is designed to put an end to this cycle.

|

|

|

|

|

| |

| A simple Spring Statement |

|

|

The Chancellor’s Spring Statement on 13 March was, as promised, a low-key event.

Last autumn, Mr Hammond announced he would have only one ‘fiscal event’ each year – an autumn Budget. The Spring Statement would become a response to revised projections from the Office for Budget Responsibility (OBR).

The Treasury has had to provide an economic commentary at least twice a year since the Industry Act 1975 was passed. Many Chancellors have taken this to mean they can have two Budgets a year – one formal Budget and another informal mini-Budget.

On 13 March the Chancellor stuck firmly to the principle of one annual fiscal event and did not announce any new spending or tax measures. It still took Mr Hammond 25 minutes to deliver his speech, however, owing to 13 new consultation papers.

Amongst the consultations were several focusing on the digital economy and the loss of tax revenue, particularly from traders based outside the UK. One paper will also review “the future role of cash”, with hints that copper coins and the £50 note may not survive much longer.

|

|

|

|

|

| |

| A turbulent February for stock markets |

|

|

February saw a dramatic return of volatility to global stock markets.

On Friday 2 February, after most of the world’s share markets had finished for the week, the Dow Jones Index dropped by 666 points in a day. Never mind all the beastly connotations of that number, in fact it was a drop of about 2.5%. The professional’s measure of the US stock market, the S&P 500, fell 2.1%.

As might be expected, the following week was unsettled, with the Dow losing over 1,000 points on both Monday and Thursday and other global equity markets experiencing similar shocks.

There were a variety of suggestions about the sudden return of volatility to a market which had spent the previous year seemingly asleep. Some blamed monthly figures released on 2 February showing higher than expected US wage growth of 2.9% C. These were read as a possible inflation threat, that would prompt a more rapid rise in interest rates. The fact that such monthly figures are notoriously volatile was, for once, ignored.

Markets recovered their poise in the following weeks. However, the press’s attentions had moved on: a large fall always gains more attention than a similar rise, especially if the rise is more gradual. For long-term investors, the big picture can therefore be lost in the noise of short term headlines. For example, the performance of the main indices in the first two months of 2018:

Index |

29/12/2017 |

31/1/2018 |

28/2/2018 |

Year to Date Change |

FTSE 100 |

7687.77 |

7533.55 |

7231.91 |

-5.9% |

S&P 500 |

2673.61 |

2823.81 |

2713.83 |

+1.5% |

Euro Stoxx 50 |

3503.96 |

3609.29 |

3438.96 |

-1.9% |

Nikkei 225 |

22764.94 |

23098.29 |

22068.24 |

-3.1% |

MSCI EM (£) |

1602.278 |

1650.679 |

1622.978 |

+1.3% |

MSCI All-World ($) |

2106.89 |

2214.11 |

2140.57 |

+1.6% |

|

|

|

|

|

| |

| Reminders for the new tax year |

|

|

The start of the new tax year on 6 April marks several changes to tax and related matters that could make you richer… or poorer.

The absence of a Spring Budget does not mean that the usual raft of changes at the start of the new tax year have disappeared. Most of the important changes were announced in the Autumn Budget, in November 2017. However, Scotland has also recently approved a new set of income tax rates and bands.

Here is a list of the more important changes that take effect for 2018/19:

• The personal allowance rises by £350 to £11,850. However, the allowance will still be phased out at £1 per £2 of income over £100,000, leaving an effective 60% (61.5% in Scotland) tax band for between £100,000 and £123,700.

• The higher rate threshold will rise by £1,350 to £46,350.

• Scotland will see several changes to income tax. A new ‘starter rate’ of 19% applies to the first £2,000 of taxable income and an ‘intermediate rate’ of 21% applies to taxable income between £12,150 and £31,580. The higher rate threshold will increase by £430 to £43,430 and the higher rate will rise by 1% to 41%.

• National Insurance Thresholds rise, with the starting point for Class 1 (employers and employees) and Class 4 (self-employed) becoming £8,424 a year. For employees and the self employed the upper limit for full rate contributions will also rise in line with the non-Scottish higher rate threshold (to £46,350).

• The dividend allowance will fall from £5,000 a year to £2,000 a year, reducing a higher rate taxpayer’s net income by up to £975.

• Company car scale rates will generally rise by 2% for petrol vehicles and 3% for diesels. The proportionate increase in tax can be more than those numbers suggest. For example, on a BMW 320d the charge rises from 24% to 27%, increasing the tax payable by one-eighth.

• The pension lifetime allowance will increase for the first time since 2010, albeit only by £30,000 to £1,030,000.

• Pension automatic enrolment minimum contributions will rise. In most instances that will mean a doubling for employers and a 150% increase for employees.

|

|

|

|

|

| |

| A refund for power of attorney |

|

|

You may be due a refund if you have registered a power of attorney in recent years.

It is not often the government offers a refund because of overcharging, but last month it emerged that the Office of the Public Guardian (OPG) had been levying excessive fees for four years. The fees related to the cost of registration of a power of attorney, whether it was an enduring power of attorney or either of its lasting power of attorney successors – dealing with health and welfare or property and financial matters.

The OPG was meant to cover its costs with attorney registration charges, but instead ended up with an £89 million surplus. As such, this sum is being returned to those who registered a power in England or Wales between 1 April 2013 and 31 March 2017. The maximum refund is £54, and most claims can be made via an online form at www.gov.uk/power-of-attorney-refund.

If the person who granted the power of attorney has died, then that individual’s executor must make a claim by email. Figures obtained via a Freedom of Information request show that up to 1.8 million people may be due a refund.

|

|

|

|

|

| |

| An improvement to the ISA inheritance rules |

|

|

The rules for inheriting ISAs will change from 6 April.

It was announced by George Osborne in 2014 that ISAs would become inheritable by surviving spouses and civil partners. At the time, nobody – not even the Treasury – was clear what the then chancellor meant.

The plans for ISA ’inheritance’, when they eventually emerged, were far from simple. Although a surviving spouse or civil partner could effectively take over the investments in their deceased partner’s ISA, the process revolved around the ISA’s value at the date of death, not when the transfer took place.

To make matters worse, the ISA tax rules ceased to apply at death, but started up again once the survivor’s inherited ISA was in place. It made an administratively complex structure of a straightforward idea.

Last November regulations were approved to simplify the process considerably, thanks to much lobbying and a protracted development of legislation. Now, for deaths occurring after 5 April 2018, in most circumstances:

• The ISA tax advantages of UK income tax and capital gains tax exemptions will continue throughout the period of estate administration.

• The inherited ISA can include any increase in value during that period.

|

|

|

|

|

| |

| Dividends expected to slow after strong 2017 |

|

|

A recently released report shows dividend payments in the UK grew more than 10% in 2017.

The report included good news for investors, as UK listed companies paid out £94.4 billion of dividends in 2017. This was up 10.5% on the previous year and a new record. However, the headline figures do not tell the whole story:

• In the final quarter of 2017 year-on-year dividend growth was just 1.1%.

• The top five dividend payers accounted for £36 out of every £100 paid, with the next ten delivering £24. The rest of the market made up the remaining £40, emphasising the concentration of dividend payers.

• Nearly half of all special dividends – one-off payments often associated with mergers or asset sales – was attributable to National Grid’s UK gas distribution disposal, totalling £6.7 billion.

• Dividends (excluding special payments) from the Top 100 companies grew by 10.0%, while the Mid 250 achieved a 14.6% increase.

• The strongest dividend growth came from the mining sector, with an increase of 162%. There was an element of smoke and mirrors about this as some big mining firms that had suspended dividends in the commodity downturn – such as Glencore and Anglo American – resumed payouts.

|

|

|

|

|

| |

| PRIIPS – the latest acronym for retail investors to learn |

|

|

New regulations are producing some strange figures in investor information documents.

There is a new acronym causing furrowed brows among investment managers, financial advisers and regulators: PRIIPS. PRIIPS are ‘Packaged Retail and Insurance-based Investment Products’, which includes most fund and investment-related products aimed at retail investors. Since 1 January 2018, a new set of EU regulations have set out what a new Key Information Document (KID) must tell potential PRIIP investors.

The idea behind KIDs is a sensible one. For some years collective funds, such as unit trusts, have had to produce a KIID (Key Investor Information Document), but there was no equivalent document for other personal investment products. This meant comparisons between different products were somewhere between difficult and impossible. The new KID was designed to provide a common set of information on risks, performance scenarios, costs and other factors in a standardised way. The aim was to make investors’ lives easier.

In practice there have been some glitches. Firstly, the transitional rules mean that KIIDs (not KIDs) can still be provided by investment managers until the end of 2019. The extra “I” adds plenty of difference – for example the old KIID includes past performance data, whereas the new KID does not. To make matters worse, the new KID rules can produce some strangely optimistic numbers covering four future ‘performance scenarios’. |

|

|

|

|

| |

| HMRC counts the cost of tax reliefs |

|

|

HMRC has published its annual assessment of the cost of tax reliefs.

Every January HMRC publishes a table of ‘Estimated costs of principal tax reliefs’. Any Chancellor facing a budget deficit is bound to run his eyes down the list to see where the money is not coming in. After that assessment, they may well ponder whether some tweaking could benefit the Exchequer’s coffers without causing too much of a political outcry.